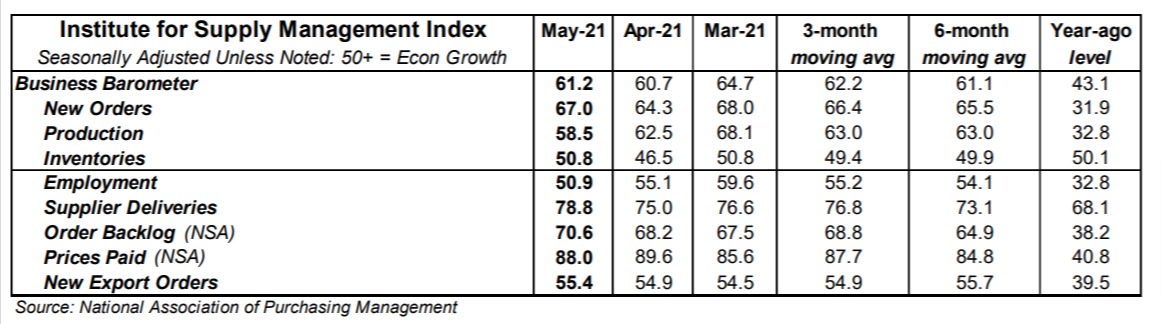

- The ISM Manufacturing Index rose to 61.2 in May, narrowly beating the consensus expected 61.0. (Levels higher than 50 signal expansion; levels below 50 signal contraction.)

- The major measures of activity were mixed in May, though all stand above 50, signaling growth. The production index fell to 58.5 from 62.5 in April, while the new orders index increased to 67.0 from 64.3. The employment index fell to 50.9 from 55.1, and the supplier deliveries index rose to 78.8 from 75.0 in April.

- The prices paid index declined to 88.0 in May from 89.6 in April.

Implications: The manufacturing sector continued to expand rapidly in May, growing slightly faster than the rapid pace in April. Gains were broad-based, with sixteen of eighteen industries reporting growth. Although a measure of current output (the production index) notched its second consecutive decline and now sits under 60 for the first time in eleven months, future output looks healthy with the new orders index jumping to 67.0 and new export orders notching a gain as well. Respondent comments were generally positive but tempered by widespread worries about disrupted supply chains, rapidly rising costs for inputs, shortages of raw materials across the board, and employers having trouble filling open positions. These issues have all come together to keep production from rising quickly enough to meet the explosion of demand as the US economy reopens. The result has been increasing delays in supplier deliveries, with the index for that measure rising to the highest level since the late 1970s. We can also see supply-chain issues in other parts of the report: the customers’ inventories index is at the lowest reading on record while the backlog of orders index (which show orders rising faster than production can fill them) at the highest reading on record. The good news is that manufacturing activity should remain robust for the foreseeable future to clear this order backlog. However, the ongoing the race to get the needed inputs to fill these orders has caused elevated readings for the prices paid index, which remains near the highest levels since 2008. Overall, seventeen of eighteen industries reported increased prices for raw materials in May. Only one commodity (acetone) was reported as lower in price while fifty-three were reported up. Inflation looks likely to remain a key topic in 2021, with the M2 money supply up 18.0% over the last twelve months at the same time supply chains struggle to catch up to demand. Finally, the employment index moved lower for a second consecutive month in May, falling to 50.9, as difficulty finding qualified workers and ongoing absenteeism issues remained headwinds. In other news this morning, construction spending rose 0.2% in April (+0.7% including revisions to prior months), below the consensus expected gain of 0.5%. The gain in April was largely due to a big increase in home building, which more than offset declines in public safety, transportation, and power projects.