If you’ve read our two most recent Monday Morning Outlooks, you know we raised our forecast for the S&P 500, but lowered our forecast for real GDP growth. How can that be?

The first thing to recognize is that when we say we’re bullish on stocks that doesn’t mean we think the stock market is going to go up every day, every week, or even every month. It won’t. Nor does it exclude the possibility of a correction in equities, which based on historical frequency is past due.

We take a fundamental approach, valuing time in the market over trying to time the market. Corrections will happen from time to time, and we don’t know anyone who can accurately forecast them on a consistent basis.

Without digging deeply into our capitalized profits model which estimates a fair value for stocks as a whole, we remain bullish for three main reasons. First, long-term interest rates are low and are likely to remain relatively low for at least the next year. Second, corporate profits are very high and will remain relatively high even if they pull back from record highs as the amount of government “stimulus” wanes.

Third, even if real (inflation-adjusted) GDP growth falls short of consensus expectations in the next few years, nominal GDP (which includes both real GDP growth and inflation), should remain robust due to the Federal Reserve’s overly loose monetary policy – see point one above – which will remain extremely loose even as the Fed starts tapering later this year and ends quantitative easing around mid-2022.

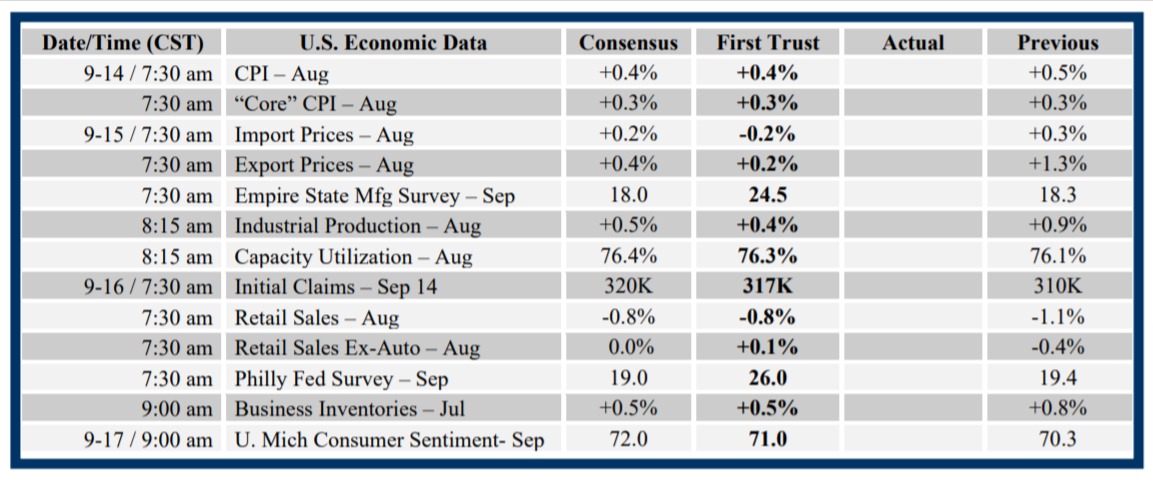

The key problem for real GDP is that the massive and unsustainable fiscal stimulus and income support that happened during COVID pushed retail sales well above the pre-COVID trend. Retail sales in July were 17.5% above the level in February 2020. To put that in perspective, in the seventeen months before COVID, retail sales were up 5.1%. There is only one way retail sales can grow 3x its normal rate while millions are unemployed and the economy was locked down – the government pulled out the credit card.

Those handouts are now slowing down and retail sales likely dropped in August (official data to be reported Thursday morning) and are likely to moderate from the 17.5% peak growth rate, on a trend basis, for at least the next year.

Retail sales make up about 30% of GDP. So other sectors of the economy will need to pick up the slack – replenishing inventories, home building, and the consumption of services, such as travel and leisure activities. But, after such massive artificial stimulus, it will be difficult for real GDP to keep growing as it has in the past nine months.

GDP includes revenues that are earned by publicly traded companies, but it also includes Main Street businesses that are not listed. It is those latter businesses that have been hurt the most by lockdowns. That’s one reason listed-company profits and their stock prices have outperformed the economy.

The bottom line is that we are bullish for now, but fully recognize that we have been in a pristine environment for stocks. A slowdown in GDP will likely slow profit growth, while rising inflation will eventually lift long term interest rates. Tax hikes are still a threat, as are tougher COVID-related restrictions that limit a service-sector recovery. However, with the Fed as easy as it is, the tailwinds from easy money remain strong. The market is not overvalued, but it is not as undervalued as it once was.